Mutual Funds’ Investments : Buyback of Shares

Buyback of Shares

What is Buyback of Shares?

Buyback of shares refers to a company's repurchase of its own shares from existing shareholders. This reduces the number of outstanding shares in the market, which can increase the value of remaining shares and provide liquidity to investors. The company usually offers a price higher than the current market price to encourage participation.

Why Do Companies Buy Back Shares?

A company may decide to buy back its shares for several reasons:

Increase Share Value : With fewer shares in circulation, earnings per share (EPS) improve, potentially boosting the stock price.

Utilizing Surplus Cash : Instead of paying dividends, companies use extra cash to buy back shares.

Prevent Hostile Takeovers : By reducing public ownership, companies can protect themselves from external control

Increase Promoter Holding : Promoters may use buyback to strengthen their stake in the company.

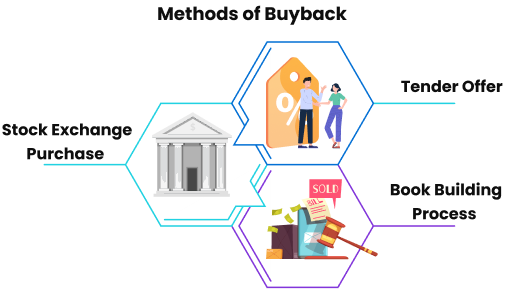

Methods of Buyback

A company can buy back shares through the following methods:

Tender Offer : Shareholders are invited to sell their shares at a fixed price, usually at a premium to the market price. A portion (15%) is reserved for small shareholders (holding shares worth up to Rs. 2 lakh).

Stock Exchange Purchase : Shares are bought directly from the stock market through brokers. However, this method is being phased out and will not be allowed after April 1, 2025.

Book Building Process : – Investors place bids within a price range, and shares are bought at the discovered price. Only listed companies can use this method

Regulations and Procedures

Buybacks are governed by SEBI (Buy-back of Securities) Regulations, 2018 for listed companies and Companies Act for unlisted companies. Key regulations include:

A company cannot buy back more than 25% of its paid-up capital and free reserves.

The buyback must be authorized by company’s Articles of Association.

If the buyback is less than 10% of net worth, only board approval is needed; otherwise, a special resolution by shareholders is required.

Public Announcement – The company must announce buyback details in newspapers and electronic media

The buyback must be completed within 1 year from approval.

Shares repurchased are extinguished (canceled) and cannot be reissued.

Important Terms for Retail Investors

A company may decide to buy back its shares for several reasons:

Tendering Shares : If participating in a tender offer, investors submit their shares through their broker or demat account.

Record Date Eligibility : Only those holding shares as of the record date can participate..

Price Consideration : Not all shares may be accepted; unaccepted shares remain in the investor’s account.

Payment and Settlement : – Accepted shares are debited, and payment is credited within 5 working days.

Benefits for Investor :

Investors may get a premium price for their shares.

Reduces floating shares, potentially increasing the stock price.

Risks for Investor:

No guarantee that all tendered shares will be accepted.

Stock price may fall after the buyback offer.